Break-Even Analysis: Key Concepts for Business Success

It’s one of the most important questions when starting out in hospitality.

“When will the business break even?”

It’s a question that’s relevant to businesses of all kinds in this sector, no matter their size. The good news is that, when you hit break even, you’re probably growing; it’s a massive step forward.

Breaking even can mean the difference between your business flourishing or disappearing without trace, and that’s what makes break-even point analysis so important.

If you haven’t heard of it, this form of analysis essentially helps you:

- determine fixed costs such as rent;

- get a handle on your variable costs (for instance, ingredients);

- set the right prices for your services; and

- gain a better understanding of when you might begin to make a profit.

Consider this your go-to guide for break-even point (BEP) analysis in hospitality.

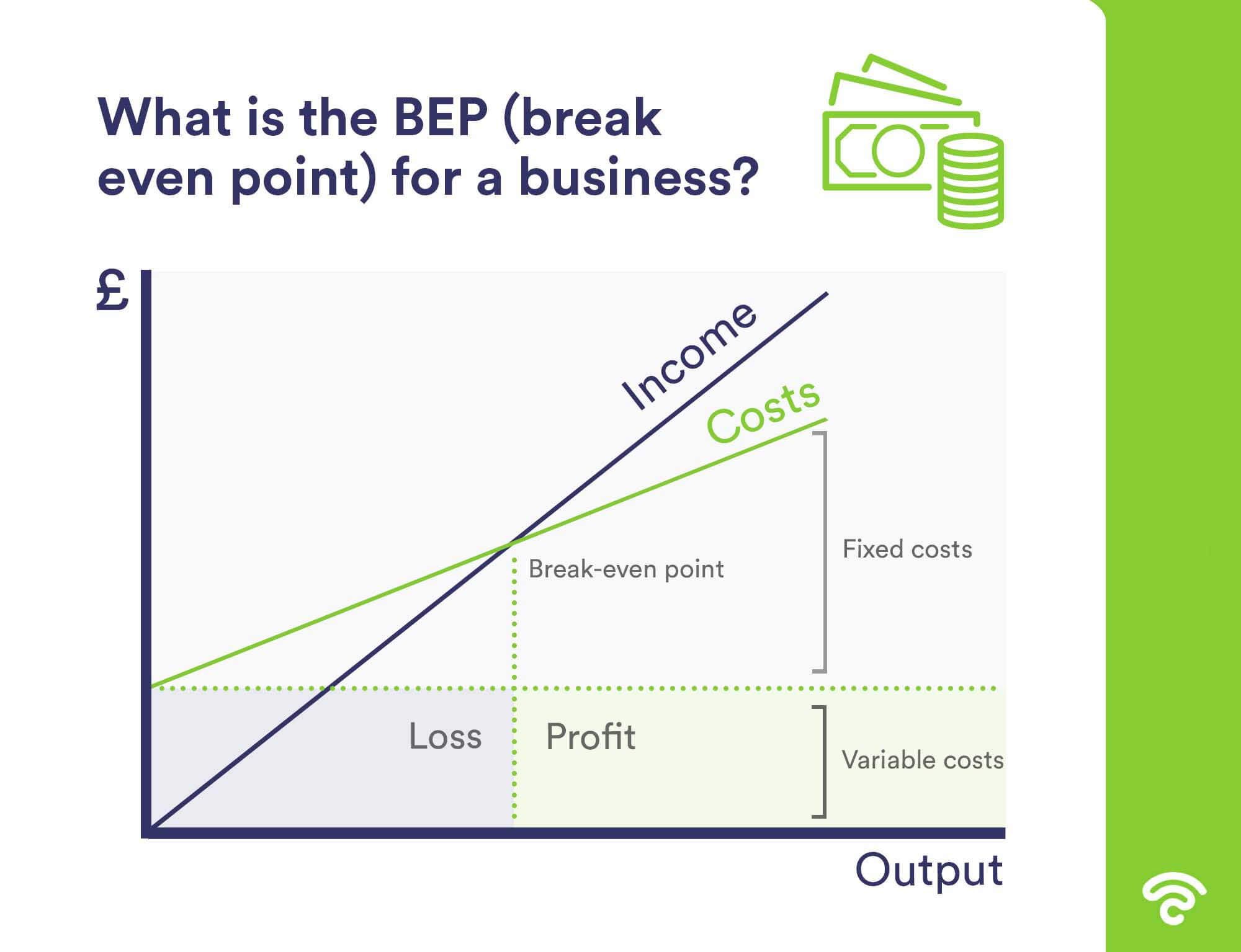

What is the BEP for a business?

Put simply, the break-even point for a business is when the costs and revenues are the same. No profit is being made, but, equally, neither are any losses.

It’s a vitally important time, because it firstly demonstrates growth; from the outset, you’ll probably have been making a loss - particularly in hospitality. Secondly, breaking even means all the hard work you put into designing your product and its pricing appears to be having a positive effect.

It’s what you do next which will make or break your business.

The simplest break-even point calculation you’ll find

There are lots of methods you can use to calculate your BEP, but the simplest is definitely the one to go for in hospitality, thanks to the relatively consistent fixed and variable costs.

The formula goes like this:

BREAK EVEN QUANTITY = FIXED COSTS / (SALES PRICE PER UNIT - VARIABLE COST PER UNIT)

The variables above are as follows:

- FIXED COSTS: your overheads that never change, regardless of how busy you are (for instance, your WiFi system)

- SALES PRICE PER UNIT: the price at which you sell something (for instance, a main dish)

- VARIABLE COST PER UNIT: how much it costs to create the product (for instance, the total cost of the ingredients for that main dish)

It might be helpful to note that the figure you arrive at after subtracting your variable cost per unit from the sale price per unit is known as the ‘contribution margin’.

For example, if you sell a dish for £20 and its variable costs are £5, the contribution margin per dish is £15, and it’s that amount which will contribute to offsetting the fixed costs. From there, you can work out your contribution margin ratio, which is usually expressed as a percentage.

The ratio is calculated by dividing your contribution margin by sales (so, if our sales are £10,000 in the example above, the ratio for that product would be 0.0015% - i.e. the percentage it contributes to reaching BEP). This will help you determine what you’ll need to do in order to break even, such as increasing prices or cutting production costs.

Let’s look at some alternative calculations.

Break-even point analysis: calculating by units

Let’s consider Sarah, who runs a coffee shop. She has already determined that the total of her fixed annual costs (which include rent, taxes and salary) are £25,000. The variable costs associated with producing one takeaway cappuccino is £0.50, and it’s sold at £2.80.

The calculation for BEP by unit is:

BEP (UNITS) = FIXED COSTS / CONTRIBUTION MARGIN

Remember:

CONTRIBUTION MARGIN = SALE PRICE OF PRODUCT - VARIABLE COSTS

So, here’s how Sarah can calculate her BEP by unit:

£25,000 / £2.30 = 10,870

So, Sarah will need to sell nearly 11,000 cups of takeaway cappuccino before she breaks even.

Puts things in perspective, right?

Break-even point analysis is typically performed at unit level just like this, and provides the business with a highly detailed view of the BEP for every sale. By subsequently multiplying and extrapolating those figures across a period of time, the business’s overall BEP can easily be identified.

Break-even point analysis: an alternative calculation (revenue)

So far, we’ve looked at BEP analysis by working at a per-unit level, but there’s another way to calculate your BEP: based on your revenue.

This is where the contribution margin comes in (remember to check our glossary of terms at the bottom of this post if it’s all getting a bit much). To calculate your BEP based on sales, do the following:

BEP (REVENUE) = SALE PRICE x BEP (UNITS)

So, here’s Sarah’s calculation for BEP based on revenue:

£2.80 x 10,870 = £30,436

Therefore, she’ll have to sell £30,436 worth of cappuccinos to break even.

5 questions to ask yourself before reaching break-even

When you’ve undertaken your BEP analysis, there are five questions you should ask yourself:

- When will we most likely break even?

- Are my prices too high to reach the break-even point before it’s too late?

- Are my costs too high to reach the break-even point before it’s too late?

- Are there any specific products that are wildly affecting the arrival of the BEP?

- Will the business be sustainable based on the calculation?

What do to with your BEP

Calculating your BEP is just the start, but it gives you a wonderful base from which to work.

Once you’ve crunched the numbers, it’ll help you analyse your plan to see if you need to cut costs, raise prices or undertake a mixture of both. It’s important to remember, however, that there’s no guarantee you’ll hit the number of products you need to sell in order to break even.

Your BEP can be used on a daily basis to help you manage the following:

- Pricing: if you’re not going to hit your BEP within an acceptable timeframe, do they need to be raised?

- Cost of goods: BEP too far away? Maybe you need to review your suppliers and raw ingredients costs.

- New menus and services: before bringing on a new dish or service, use its fixed and variable costs to see how it’ll impact your BEP.

- Planning: if, for instance you want to expand, you can add the increased fixed and variable costs to your BEP calculations to see how it’s impacted.

At its base level, your BEP analysis can work as a brilliant tool to keep the team motivated and your goals realistic. It’s much easier to retain a sense of perspective if you know how long it’ll take to break even and start making money.

When should I conduct a BEP analysis and what should I be aware of?

Break-even point analysis should ideally take place when you start the business and should form part of your business plan. However, it can - and should - be undertaken in existing businesses, too.

Just bear in mind that the analysis assumes you’ll sell everything in time, and that might not happen. Equally, it doesn’t take into account external events or those which are out of your control (such as an economic downturn or unexpected arrival of a competitor).

In hospitality, some variable costs aren’t static, either. For instance, the cost of food production might momentarily reduce if you’re able to buy a specific ingredient in bulk for a short period of time.

It’s for these reasons that you shouldn’t treat BEP analysis as gospel - more a guiding light and goal to which you can aim all of your efforts.

Glossary of terms

We appreciate this can get a bit confusing if you’re only just starting out, but if you familiarise yourself with the following terms, you’ll slowly get your head around the intricacies of BEP.

- Break-even point. When your total sales equals your fixed and variable costs, you’ve reached break even.

- Fixed costs. These are costs that never change, regardless of how much stuff you sell. Examples include rent, equipment leases and the fees you pay on services such as advertising.

- Variable costs. These do change, depending on your output. Typical variable costs in the hospitality industry include utility bills, raw ingredients and wages.

- The contribution margin. You reach this figure by subtracting an item’s variable costs from its selling price. The result is a monetary value that indicates how much that item contributes towards covering your fixed costs every time it’s sold. If there’s anything left over, that’s net profit.

- Contribution margin ratio. A percentage that’s calculated by dividing your contribution margin by sales. It’s great for helping you working out what needs to be done to break even.

Recommended further reading: The Handy Guide to Average Restaurant Profit Margins

Recommended further reading: How to Identify Needless Costs in Your Hospitality Business

Get Started With Free WiFi Marketing

Beambox helps businesses like yours grow with data capture, marketing automation and reputation management.

Sign up for 30 days free